Business

Signs global bond markets could be bottoming out after central bank rate hikes

Fixed-income investors are experiencing what could be the most challenging year for bond markets in 45 years, with 2022 shaping up to be possibly the worst since 1931.

Bonds are units of debt issued by companies or governments that are converted into tradable assets. They contain the loan terms, such as the interest payment, bond principal, and maturity date. Bonds essentially function as instruments used by governments and corporations for borrowing money. Although the stock market generates far more headlines, global bond markets are much larger in value than stock markets, with more than $100 trillion tied up in bonds worldwide versus $64 trillion in equities.

Investors generally demand higher interest rates for lending to governments over extended periods, reflecting the opportunity cost of tying up their money longer amid rising growth and inflation forecasts. On the other hand, short-term rates occasionally rise beyond longer-term yields, disturbing the bond markets’ usual trend. When the yield curve inverts, investors demand more interest to lend to the government over shorter periods. This abnormality implies that investors anticipate economic growth to decline soon. Historically, an inverted yield curve has been a strong indicator of a pending recession. This is especially true when the U.S. faces strong global headwinds from Europe, where the Russia-Ukraine war and related sanctions have created a painful energy price shock.

Many consider bonds safer alternatives to other investments, and Treasury bonds are among the safest government bonds. While bonds are less volatile and tend to outperform equities in times of economic hardship, this does not imply that they are a rock-solid investment or that you should only invest in bonds.

Olive Invest collected information about bond markets from various professional, expert, and news sources to paint a clearer picture of the U.S. bond market’s performance.

![]()

MDart10 // Shutterstock

Interest rates continue to increase, but at a slower pace

Two years into the worst pandemic in a century, the global economy still struggles with the COVID-19 pandemic’s lingering effects of diminishing economic growth and soaring prices. Specifically, the U.S. has been battling inflation since the economy picked up after COVID-19-related shutdowns of industries and disrupted supply chains. To curb inflation, the Federal Reserve has leveraged the tools at its disposal, primarily interest rate hikes and the threat of more. Most recently, the Fed hiked interest rates by 75 basis points. However, the pass-through effect on the bond market could cause bond prices to bottom out.

At first glance, the relationship between interest rates and bond prices might not be apparent. But upon closer examination, it becomes clear that when central banks hike interest rates, bond prices fall, ensuring the face value of the bond remains constant. This is known among future brokers studying for their securities licensing exams as the teeter-totter, likening bond prices and interest rates to a seesaw on a children’s playground. Because of the inverse relationship between interest rates and bond prices, a further decline in bond prices can be expected as the Fed continues to hike interest rates.

larry1235 // Shutterstock

Stock market volatility driven in part by risks from Europe cause investors to seek safe havens like Treasury bonds

Ideally, equity markets offer higher expected returns than fixed-income markets. However, they also carry higher risks of loss. The Fed’s aggressive rate hikes and the risks of emerging market bond defaults have combined with energy crisis-related factory furloughs in Germany and other European manufacturers to spook investors. The result has been a flight to safety, with institutional and individual investors turning to Treasury bonds.

Lower bond prices have begun to present lucrative opportunities for investors seeking yield but with safety. Short-term instruments currently offer rising yields at 4.48% for six months, 4.53% for one year, and 4.41% for two years, while longer maturities like the five- and 10-year bonds offer yields of 4.18% and 4.01%, respectively.

corlaffra // Shutterstock

Recession talk from business and political leaders pushes stocks lower, likely sending bonds higher

As the Fed maintains its hawkish stance and Fed Chairman Jerome Powell indicates it will continue to hike rates aggressively, industry experts and investors are worried it may push the U.S. economy into recession.

The last time the Fed hiked rates aggressively to curb inflation was during the early 1980s under then-Fed Chairman Paul Volcker. The Volcker Fed rate hikes made borrowing money and mortgage rates so expensive that bank certificates of deposit insured by the Federal Deposit Insurance Corporation were yielding 18% in May 1981, close to the high-water mark of the severe recession of 1981-82.

Regarding the present outlook, Fed officials have stated that they want to keep raising interest rates well above the current range of 3% to 3.25%, leaving analysts to speculate how high rates could go. However, the costs of servicing global debt burdens governments have accrued over the last 40 years across the G7 nations, including the U.S., would make any Fed rate hike approaching those interest rates Americans witnessed in the early 1980s unbearable.

With interest rates rising faster than expected, the unanticipated impacts of quantitative tightening and the expected prolonged war in Ukraine are indicators analysts believe are likely tipping the U.S. economy into recession. Against this stark global backdrop, industry experts, such as JPMorgan Chase CEO Jamie Dimon, believe the S&P 500 could suffer a painful downturn. A negative outlook for the equity markets may drive investors, in turn, back into the fixed-income markets, resulting in higher bond prices.

This story originally appeared on Olive Invest and was produced and

distributed in partnership with Stacker Studio.

Inflation has cooled substantially, but Americans are still feeling the strain of sky-high prices. Consumers have to spend more on the same products, from the grocery store to the gas pump, than ever before.

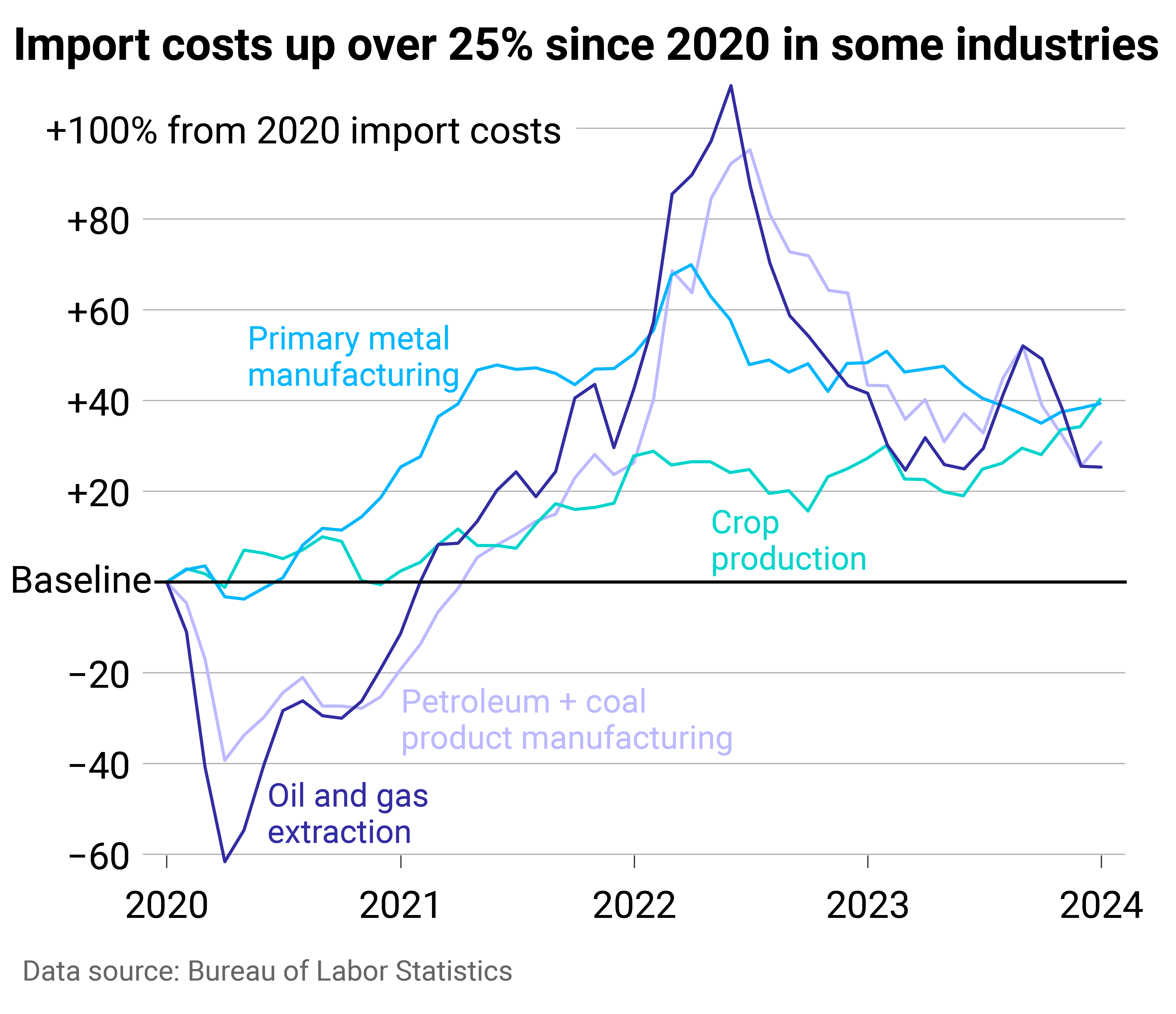

Increased import costs are part of the problem. The U.S. is the largest goods importer in the world, bringing in $3.2 trillion in 2022. Import costs rose dramatically in 2021 and 2022 due to shipping constraints, world events, and other supply chain interruptions and cost pressures. At the June 2022 peak, import costs for all commodities were up 18.6% compared to January 2020.

While import costs have since fallen most months—helping to lower inflation—they remain nearly 12% above what they were in 2020. And beginning in 2024, import costs began to rise again, with January seeing the highest one-month increase since March 2022.

Machinery Partner used Bureau of Labor Statistics data to identify the soaring import costs that have translated to higher costs for Americans. Imports in a few industries have had an outsized impact, helping drive some of the overall spikes. Crop production, primary metal manufacturing, petroleum and coal product manufacturing, and oil and gas extraction were the worst offenders, with costs for each industry remaining at least 20% above 2020.

![]()

Machinery Partner

Imports related to crops, oil, and metals are keeping costs up

At the mid-2022 peak, import costs related to oil, gas, petroleum, and coal products had the highest increases, doubling their pre-pandemic costs. Oil prices went up globally as leaders anticipated supply disruptions from the conflict in Ukraine. The U.S. and other allied countries put limits on Russian revenues from oil sales through a price cap of oil, gas, and coal from the country, which was enacted in 2022.

This activity around the world’s second-largest oil producer pushed prices up throughout the market and intensified fluctuations in crude oil prices. Previously, the U.S. had imported hundreds of thousands of oil barrels from Russia per day, making the country a leading source of U.S. oil. In turn, the ban affected costs in the U.S. beyond what occurred in the global economy.

Americans felt this at the pump—with gasoline prices surging 60% for consumers year-over-year in June 2022 and remaining elevated to this day—but also throughout the economy, as the entire supply chain has dealt with higher gas, oil, and coal prices.

Some of the pressure from petroleum and oil has shifted to new industries: crop production and primary metal manufacturing. In each of these sectors, import costs in January were up about 40% from 2020.

Primary metal manufacturing experienced record import price growth in 2021, which continued into early 2022. The subsequent monthly and yearly drops have not been substantial enough to bring costs down to pre-COVID levels. Bureau of Labor Statistics reporting shows that increasing alumina and aluminum production prices had the most significant influence on primary metal import prices. Aluminum is widely used in consumer products, from cars and parts to canned beverages, which in turn inflated rapidly.

Aluminum was in short supply in early 2022 after high energy costs—i.e., gas—led to production cuts in Europe, driving aluminum prices to a 13-year high. The U.S. also imposes tariffs on aluminum imports, which were implemented in 2018 to cut down on overcapacity and promote U.S. aluminum production. Suppliers, including Canada, Mexico, and European Union countries, have exemptions, but the tax still adds cost to imports.

U.S. agricultural imports have expanded in recent decades, with most products coming from Canada, Mexico, the EU, and South America. Common agricultural imports include fruits and vegetables—especially those that are tropical or out-of-season—as well as nuts, coffee, spices, and beverages. Turmoil with Russia was again a large contributor to cost increases in agricultural trade, alongside extreme weather events and disruptions in the supply chain. Americans felt these price hikes directly at the grocery store.

The U.S. imports significantly more than it exports, and added costs to those imports are felt far beyond its ports. If import prices continue to rise, overall inflation would likely follow, pushing already high prices even further for American consumers.

Story editing by Shannon Luders-Manuel. Copy editing by Kristen Wegrzyn.

This story originally appeared on Machinery Partner and was produced and

distributed in partnership with Stacker Studio.

Nearly every state requires drivers to carry car insurance, but the laws vary, and many factors affect the cost of coverage.

Some are controllable, at least to degrees: the type of car you have and your credit history. Some are not: your age and gender. Your marital status, place of residence, and claims history are among the other variables that go into it.

Across the United States, premiums are soaring, rising 20% year over year and increasing six times faster than consumer prices overall as of December 2023, CBS reported. Last September, CNN noted that car insurance rates jumped more in the previous year than they had since 1976.

CBS pointed to many potential reasons for these increases in prices. Coronavirus pandemic-era issues have made buying, fixing, and replacing vehicles costlier. Extreme weather events caused by climate change also damage more vehicles, while insurance companies are increasing their business costs. Severe and more frequent crashes are to blame as well, CNN reported.

On top of these, local factors such as population density, the number of uninsured drivers, and the frequency of insurance claims all affect premiums, which can lead motorists to change or switch their coverage, use other modes of transportation, or even alter decisions about when to buy a vehicle or what to look for.

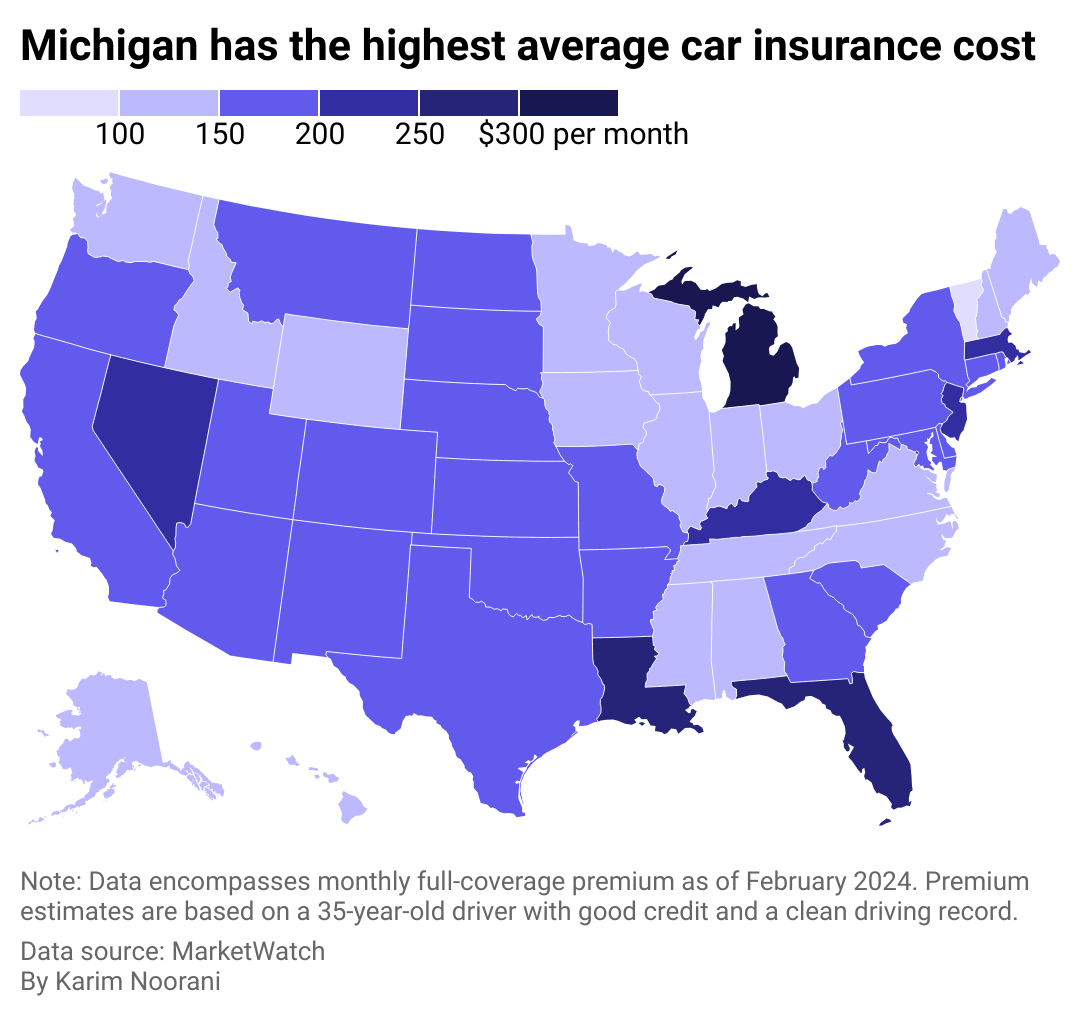

To see how geography affects cost, Cheap Insurance mapped the states where people pay the most in car insurance premiums using MarketWatch data. Premium estimates were based on full-coverage car insurance for a 35-year-old driver with good credit and a clean driving record. Data accurate as of February 2024.

![]()

Cheap Insurance

Americans pay $167 per month on average for full-coverage insurance

There are common denominators among the five states where it’s most expensive to have car insurance: Michigan, Florida, Louisiana, Nevada, and Kentucky. Washington D.C. is another pricey locale, ranking #4 overall.

Three of these six are no-fault jurisdictions and require additional coverage beyond coverage to pay for medical costs. Michigan notably calls for $250,000 in personal injury protection (though people with Medicaid and Medicare may qualify for lower limits), $1 million in personal property insurance for damage done by your car in Michigan, and residual bodily injury and property damage liability that starts at $250,000 for a person harmed in an accident.

Other commonalities between these states include high urban population densities. At least 9 in 10 people in Nevada, Florida, and Washington D.C. live in cities and urban areas, which leads to more crashes and thefts and high rates of uninsured drivers and lawsuits. Additionally, Louisiana, Florida, and Kentucky rank #5, #8, and #10, respectively, in motor vehicle crash deaths per 100 million vehicle miles traveled in 2021 based on Department of Transportation data analyzed by the Insurance Institute for Highway Safety.

Canva

#5. Kentucky

– Monthly full-coverage insurance: $210

– Monthly liability insurance: $57

Canva

#4. Nevada

– Monthly full-coverage insurance: $232

– Monthly liability insurance: $107

Canva

#3. Louisiana

– Monthly full-coverage insurance: $253

– Monthly liability insurance: $77

Canva

#2. Florida

– Monthly full-coverage insurance: $270

– Monthly liability insurance: $115

Canva

#1. Michigan

– Monthly full-coverage insurance: $304

– Monthly liability insurance: $113

Story editing by Carren Jao. Copy editing by Paris Close. Photo selection by Lacy Kerrick.

This story originally appeared on Cheap Insurance and was produced and

distributed in partnership with Stacker Studio.

Business

How businesses can protect themselves from the rising threat of deepfakes

Dive into the world of deepfakes and explore the risks, strategies and insights to fortify your organization’s defences

Dave is a journalist whose work has appeared in more than 100 media outlets around the world, including BBC, National Post, Washington Times, Globe and Mail, New York Times, Baltimore Sun.

-

Business4 months ago

Business4 months agomesh conference goes deep on AI, with experts focusing in on training, ethics, and risk

-

Business4 months ago

Business4 months agoSkill-based hiring is the answer to labour shortages, BCG report finds

-

Events6 months ago

Events6 months agoTop 5 tech and digital transformation events to wrap up 2023

-

People4 months ago

People4 months agoHow connected technologies trim rework and boost worker safety in hands-on industries

-

Events3 months ago

Events3 months agoThe Northern Lights Technology & Innovation Forum comes to Calgary next month